There is No Such Thing as “Ideal”Homeownership Rates:

But Every Neighborhood Still Needs to Ensure Equitable Pathways to Homeownership

Written by,

Seema Iyer

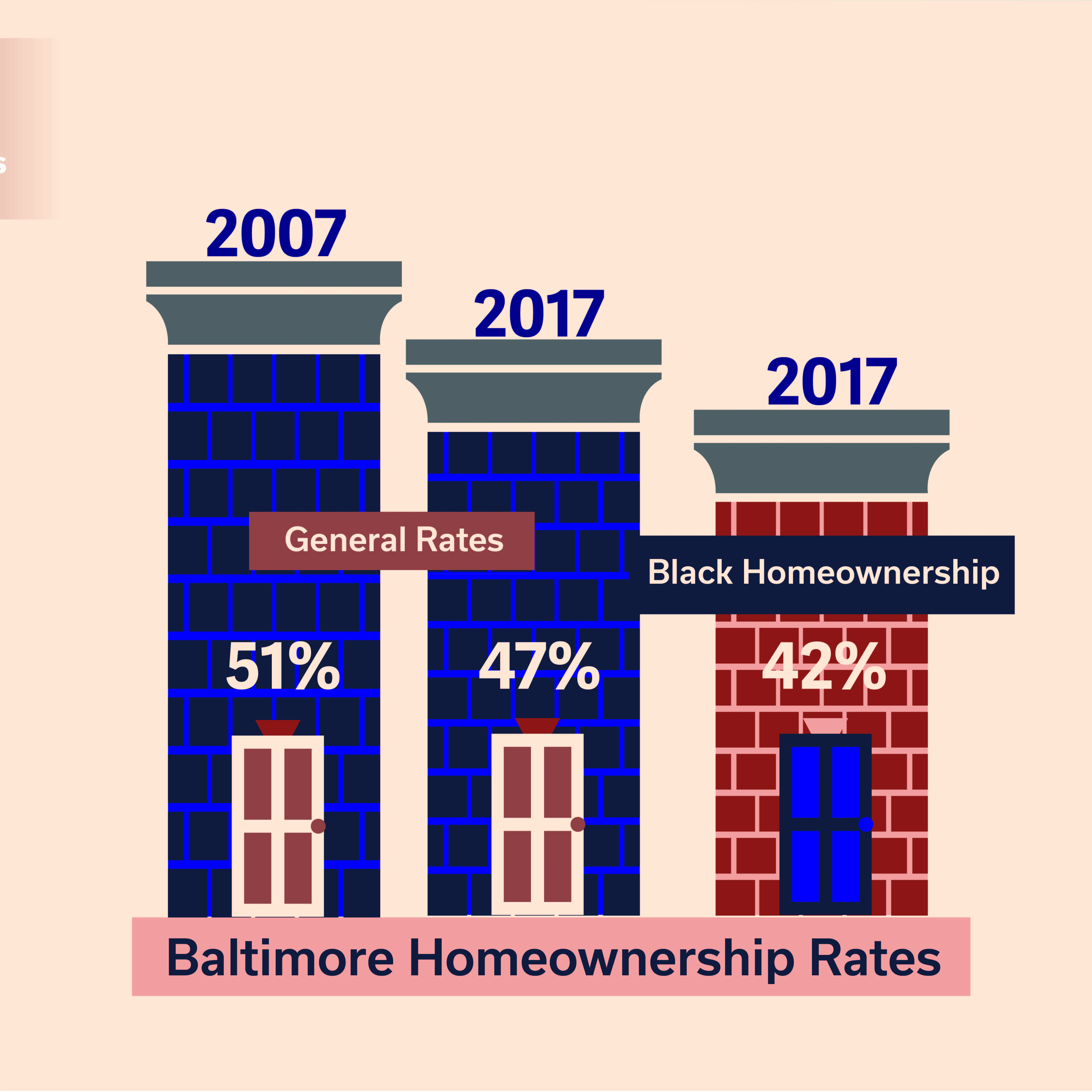

In July, the BNIA team worked with researcher Sally J. Scott, Director of the Community Leadership Programs at UMBC, to report on trends and barriers to homeownership in Baltimore’s neighborhoods. In the report, Overcoming Barriers to Homeownership in Baltimore, we found that from 2007 to 2017, the homeownership rate in Baltimore City fell from 51% to 47%, and the Black homeownership rate sank to 42%. However, even more dramatic declines (more than 12%) occurred in neighborhoods, particularly in the Southwest part of the city (Saint Paul, Irvington, and Lakeland being the specific neighborhoods with the greatest declines). These trends represent the loss of Black middle class families in Baltimore, and increasing inequality between predominantly white and predominantly Black neighborhoods.

The report identified clear recommendations for the City, housing non-profits/advocates and other institutions involved in funding and promoting homeownership, particularly with a goal of increasing Black homeownership and reducing continued racial disparities.

But after the report came out, BNIA started to get a lot of queries from neighborhood residents and leaders about what the “ideal” rate of homeownership might be, presumably as a way to set some goals and priorities for their community. The answer, of course, is that there is no such thing. We have perfectly sustainable and healthy neighborhoods in Baltimore with a broad range of ownership rates.

What the Vital Signs indicators show is that the current percentage of homeownership in any community does not alone represent a sign of sustainability; rather, it’s about how stable or fast-changing that percentage might be.

Take for example neighborhoods like Midtown or Greater Charles Village which have below-average owner-occupancy (41% and 42% respectively) and have been steady at those levels for more than a decade. What can other neighborhoods learn from areas like these?

Key Recommendation

Fast-changing owner-occupancy rates in a relatively short timeframe causes the character of a neighborhood to change in a way that neighbors can’t get a hold of. This is what is happening in those neighborhoods listed above. Some other neighborhoods like Belair Edison and Edmondson Village also have declining owner-occupancy and ironically increasing rent burden where more renters are spending more than 30% of their income on rent. That’s a problem that potentially a focus on increasing homeownership might help on multiple fronts.

So our message to neighborhoods is to use data to get “tactical”???? and more specific on how to set clear goals in the hopes of equitably increasing homeownership in the neighborhood. Here are just a few ideas to get your neighborhood started:

5 Things Neighborhood Can Do to Increase Homeownership Equitably

-

Help 10 current renters in the neighborhood form a homeownership learning cohort

Homeownership is complicated, for anyone. Several organizations that were interviewed for the Abell report offer homeownership counseling and even one-on-one coaching (Neighborhood Housing Services, LiveBaltimore, St. Ambrose Housing Aid Center–just to name a few). But research shows that by connecting participants who go through the process in a cohort, members will develop long-term relationships with whom they can share common practices and experiences, learn strategies and connect during and beyond the cohort’s planned term.

-

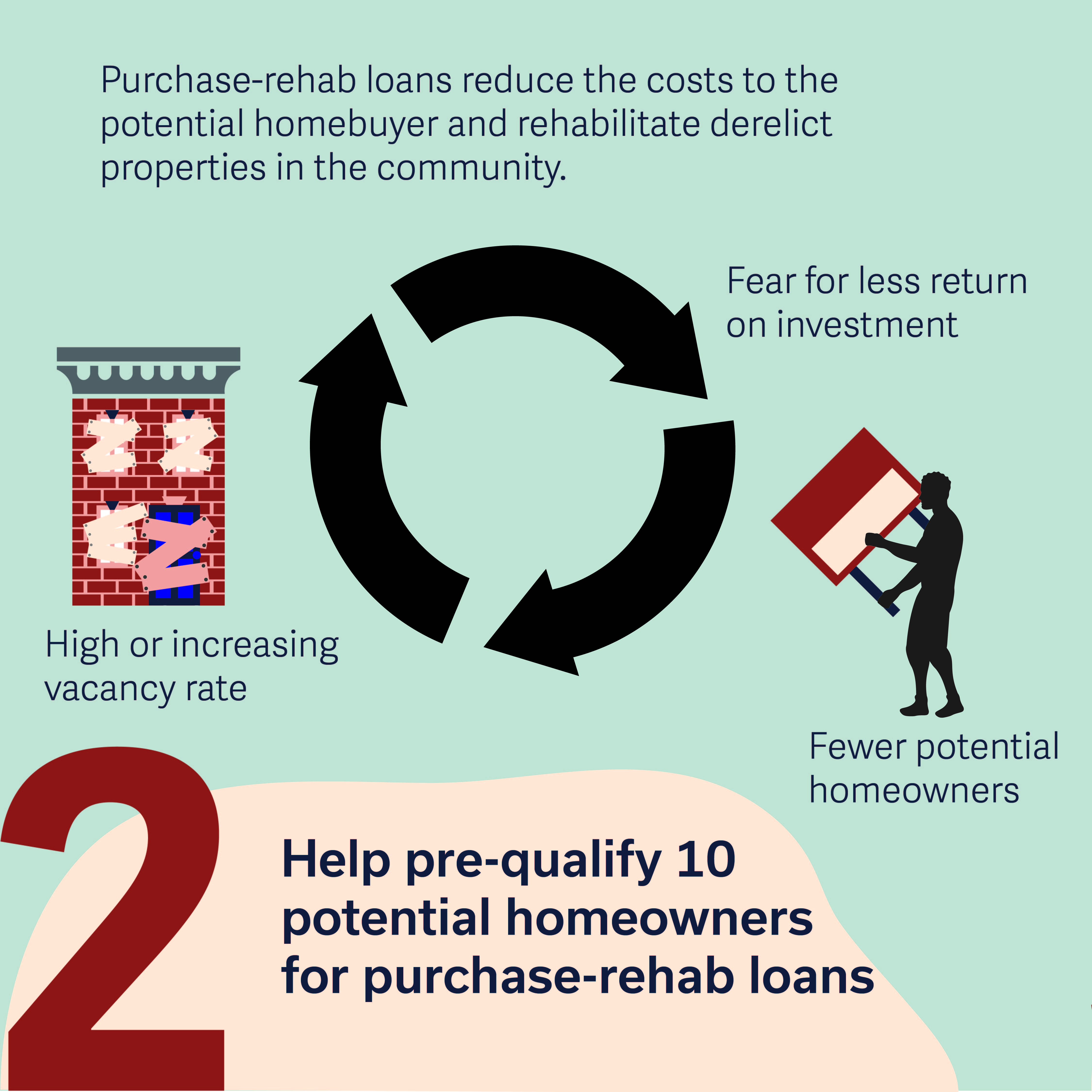

Help pre-qualify 10 potential homeowners for purchase-rehab loans

In some neighborhoods, the vacancy rate is high or is increasing which presents a problem to attract potential homeowners who fear that they may not get a return on their investment. However, organizations such as Healthy Neighborhoods have low-interest loan s that are specifically designed to both reduce the costs to the potential homebuyer as well as helping to rehabilitate derelict properties in the community. Other opportunities exist as well such as the 203K Rehabilitation Loan for qualifying homes or any lending institution that offers commercial purchase-rehab loans.

-

Identify 10 unoccupied properties for potential homebuyers to rehab

The City of Baltimore’s Housing Department has code inspectors that identify properties in neighborhoods that are no longer habitable. These properties receive a Vacant Building Notice and increasingly are part of the the Vacants to Values program to incentivize rehabilitation. However, many properties in neighborhoods are unoccupied for reasons that only neighbors would know about such as divorce, advanced age, or death of the owner. Neighborhood organizations should keep an inventory of these kinds of properties that might require extra time to transfer to new owners–ones who in the meantime are getting pre-qualified for a purchase-rehab loan!

-

Help 10 current homeowners with their estate deed plan

Homeownership retention and proper transfer of ownership are also part of the problem leading to declines in owner-occupancy. Any owner on record of a property should plan ahead for the eventual need to pass along the property to a beneficiary or a new owner. The My Home, My Deed, My Legacy project by Maryland Volunteer Lawyers Service (MVLS) helps provide estate planning services so that homeowners don’t lose their homes and, if needed, successfully pass along their home to an intended beneficiary.

-

Meet with 10 Realtors® who sell homes in the neighborhood

Get you know the real estate agents who are working in your neighborhood. They are continuously marketing properties in your area and have great intel on how well your neighborhood is doing to attract potential homebuyers. They know what kinds of upgrades are (or are not) selling, what kinds of buyers are interested in the neighborhood and even which other neighborhoods are your competition that you might learn from. If your neighborhood does not have any steady cadre of real estate agents, then it’s time tohome-grow them. Many people at all education levels can earn a steady income helping property owners sell their homes, and who better to help market your neighborhood than one of your own!

These are challenging times in Baltimore, but communities in Baltimore are still doing the daily work of keeping their neighborhoods strong and resilient. We hope these strategic, tactical and manageable recommendations will help with not only neighborhoods’ homeownership goals, but more importantly with increasing equitable housing security for everyone.